Aydın,

17°C

parçalı bulutlu

Over the past two years, artificial‑intelligence technologies have sparked a surge of capital into the tech sector. Data‑center operators, cloud providers, and the manufacturers of high‑performance chips are seeing revenues climb at rates not witnessed since the early 2000s dot‑com rally.

Companies that design and construct massive data‑center campuses are enjoying a windfall. Their suppliers—from cooling‑system engineers to power‑grid specialists—are also benefiting from record‑high demand. In many markets, the AI‑driven expansion has become the primary growth engine, dwarfing traditional drivers such as consumer electronics and retail.

While the AI sector thrives, other industries are showing signs of strain. Manufacturing output has stalled, and employment growth in non‑tech sectors remains sluggish. Analysts warn that the current boom may be masking deeper structural problems, including a slowdown in consumer spending and lingering supply‑chain bottlenecks.

Several risk factors could temper the current enthusiasm:

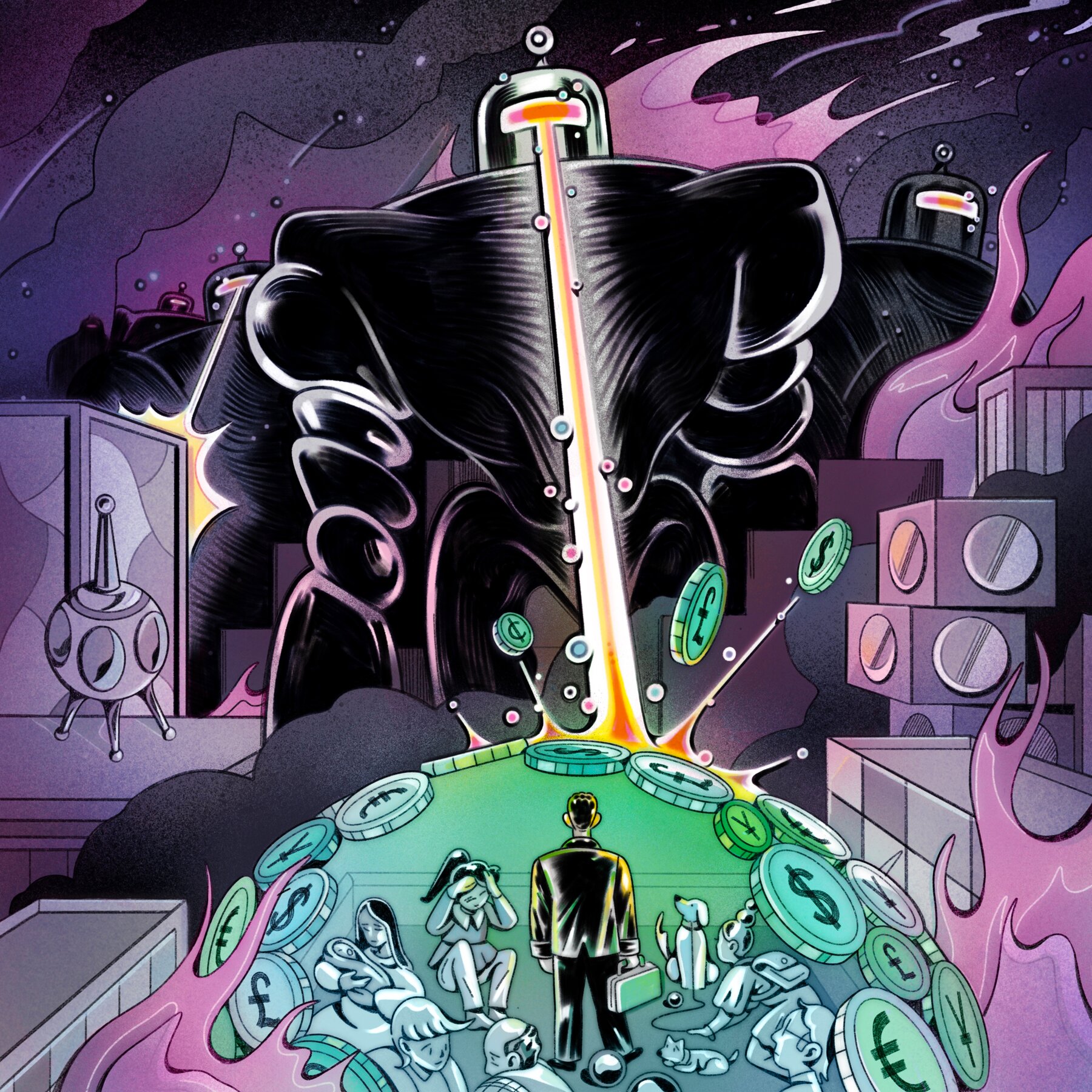

If the AI boom loses momentum, the ripple effects could be significant:

Industry leaders are already taking steps to cushion a possible downturn. Diversifying revenue streams, investing in energy‑efficient technologies, and building resilient supply chains are at the top of most CEOs’ agendas. Governments, too, are considering incentives for green‑energy integration and workforce retraining to keep the sector robust.

The AI boom has undeniably become a catalyst for economic expansion, especially for data‑center developers and their ancillary industries. However, reliance on a single growth engine carries inherent risks. Stakeholders—from investors to policymakers—must stay vigilant, prepare contingency plans, and promote a balanced ecosystem to ensure that the economy can weather a potential AI slowdown without losing momentum.